Taxes play a crucial role in government revenue. They come in two main types: direct and indirect taxes. In India, taxes apply to both citizens and income earned within the country. The Income-tax Act of 1961 regulates income earned by both residents and Non-Resident Indians (NRIs). However, there are significant differences in the tax rules for residents and NRIs. This article explores the requirements for filing Income-tax Returns and other provisions outlined in the Income-tax Act specifically for NRIs.

What’s a Non-Resident Indian (NRI)?

According to the Income-tax Act of 1961, an NRI is someone who isn’t a resident. The Act considers a person a Resident of India if they meet any of these 6 conditions:

| List of Conditions to become Resident in India on Priority Basis | ||||||

| Particulars | Purpose Based | Other than Purposes 1, 2 & 3 | Deemed Resident | |||

| Priority | 1 | 2 | 3 | 4 | 5 | 6 |

| Citizenship | Indian | Indian or PIO* | Indian or PIO | Not Relevant | Indian | |

| Purpose during the year | Leaving India for the purpose of employment or as a member of crew of Indian ship | Being outside India, comes on a VISIT | Not Relevant | |||

| Income Limit | Not Applicable | <= 15 Lakhs India sourced Incomes | > 15 Lakhs India sourced Incomes | Not Applicable | > 15 Lakhs India sourced Incomes | |

| No. of days stay in India during the year | 182 days or more | 120 days or more | 182 days or more | 60 days or more | Not Relevant | |

| No. of days stay in India during preceding 4 years | Not Applicable | 365 days or more | Not Applicable | 365 days or more | Not Applicable | |

| Resident in a country outside India | Not Applicable | No | ||||

| Note: If one satisfies all conditions in any one column, he/she would be a Resident in India for that year. |

Requirements for NRIs to Submit Income Tax Returns

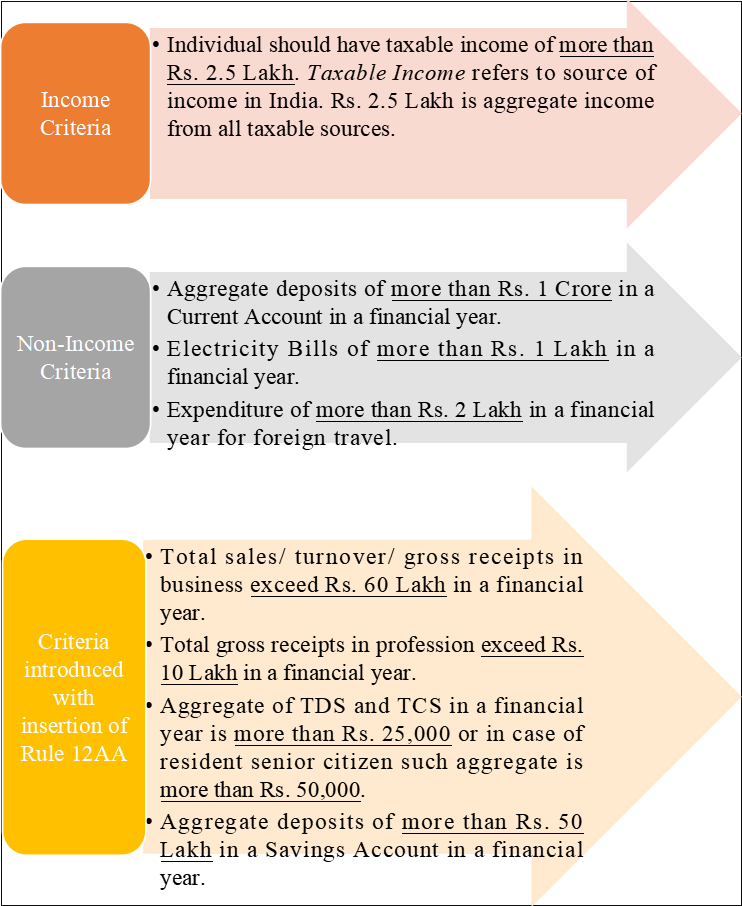

For NRIs to file their income tax returns in India, they need to meet the following criteria:

Incomes Counted in the Rs. 2.5 Lakh Threshold Limit

To calculate the total threshold limit of Rs. 2.5 Lakh, any income received, accrued, sourced, or earned in India will be subject to tax for an NRI. This includes income in the form of:

– Salary

– Business/Professional Income

– Rental/Lease Income

– Interest/Dividend Income from Shares, Mutual Funds, or Banks

– Capital Gains from the sale of Shares, Mutual Funds, Property, etc.

For example, rent received by an NRI for a property in India and salary earned for services rendered in India will be counted towards the Rs. 2.5 Lakh threshold limit.

Treatment of Exempt Income in Slab Calculation

When calculating the Rs. 2.5 Lakh threshold limit for an NRI, the following incomes will not be counted:

1. Exempt income of NRIs that isn’t taxable.

2. Interest income from Non-Resident External (NRE) or Foreign Currency Non-Resident (FCNR) accounts.

3. Any exemptions notified by the government for NRIs.

For example, if an NRI’s interest income from NRE Fixed Deposits (FDs) is Rs. 1.5 Lakh (exempt income) and all other taxable income in India is Rs. 1.5 Lakh, these two incomes don’t need to be added when computing the threshold limit. As the taxable income is below the Rs. 2.5 Lakh limit, the NRI isn’t required to file a tax return.

Treatment of Tax Deductions in Slab Calculation

When an NRI invests their income in instruments eligible for tax deductions, here’s how the threshold limit is calculated:

1. The Rs. 2.5 Lakh threshold limit is considered before applying for eligible deductions.

2. Tax deductions are applicable only when the NRI files their tax return.

So, if an NRI’s taxable income, excluding deductions, exceeds Rs. 2.5 Lakh, they should file their tax return to claim these deductions.

For example, if an NRI’s total taxable income is Rs. 3.5 Lakh and they have Rs. 1.5 Lakh in tax deductions, they should file their tax return. By doing so, they can claim the Rs. 1.5 Lakh deduction and avoid paying tax on the total income.

Income Threshold for Senior NRIs

The Rs. 2.5 Lakh threshold applies to all senior NRIs.

There are no special relaxation slabs for any category of senior NRIs.

Benefits of Filing Tax Returns (Even with NRI Annual Income below Rs. 2.5 Lakh)

1. Claim TDS Refund: You can get a refund for any excess TDS deducted.

2. Carry Forward Losses: Any losses incurred can be carried forward for future offset.

3. Prove Tax Status: Filing helps establish your tax status in India.

4. Claim Exemptions under DTAA#: You can claim exemptions under Double Taxation Avoidance Agreements, if applicable.

By filing your income tax return in India, even if your total income is below the threshold limit, you can enjoy these benefits as an NRI.

Exceptions for NRIs Not Requiring Tax Return Filing (Income Tax for Non-Resident Indians)

NRIs are exempt from filing tax returns in India under these specific conditions:

1. Solely investment income: If income solely comes from investments, specifically from Indian company securities, including interest/dividend income and capital gains from their sale.

2. Invested funds from Convertible Foreign Exchange: The invested amount must originate from convertible foreign exchange, meaning money sent from outside India.

3. Full TDS deduction: The income payer must fully deduct the applicable Tax Deducted at Source (TDS).

Conclusion

Tax rules for NRIs (Income Tax for Non-Resident Indians) differ considerably from those for resident Indians. It’s essential to grasp the specific taxation provisions outlined in the Income-tax Act, 1961, to prevent the possibility of double taxation when earning income in India and abroad. Understanding these policies aids in determining one’s residential status and accessing tax benefits accordingly. Therefore, NRIs should have a clear understanding of all taxation aspects applicable to them in India. For any queries, contact us, today!